Breaking the taste barrier: How alt-dairy can capture mainstream consumers

Key takeaways

- Alt-dairy products like barista milk now match dairy in taste, but a taste gap in dairy-free ice cream and mozzarella remains.

- The biggest challenge for plant-based brands is improving richness and reducing off-flavors in dairy-free products.

- Brands that evoke indulgence and comfort, alongside health benefits, see stronger consumer interest and repeat purchases.

Alt-dairy manufacturers can already achieve taste parity in some dairy categories — especially barista milk and creamers — but an R&D push is needed to close the taste gap in dairy-free ice cream and mozzarella, a sensory analysis of established and emerging alternative dairy companies by Nectar has revealed.

The non-profit research initiative, which evaluated taste and texture challenges in plant-based meat alternatives last year, calls its first dairy alternatives study the “largest publicly available” sensory analysis of dairy-free products to date. The study aims to accelerate the shift of the US$1.2 trillion (according to Nectar) dairy industry — which accounts for nearly 4% of all anthropogenic emissions — toward more sustainable alternatives.

The team evaluated 98 commercialized dairy-free products across ten categories with 2,183 omnivore and flexitarian consumers in San Francisco and New York City (US) between September 2025 and November 2025.

Yesterday, Nectar also announced the results of the 2026 Tasty Award Winners in San Francisco, recognizing the best alternative protein products from its latest sensory evaluations. The winners include barista milk by Califia Farms, Dream, Milkadamia, Minor Figures, Planet Oat, and Ripple; butter (salted) by Country Crock, Melt Organic, and Violife; cheddar by Field Roast, Follow Your Heart, Miyoko’s Creamery, and Plant Ahead; and cream cheese by Violife.

Creamers by Coffee Mate, Oatly, Planet Oat, Silk, Sown, and Violife; ice cream by So Delicious, milk by Blue Diamond, Maizly, and Silk; sour cream by Violife, and yogurt by Cocojune were the other winners.

Food Ingredients First speaks with Nectar’s director, Caroline Cotto, to understand how the new findings might help alt-dairy manufacturers push dairy-free products beyond niche adoption, with the data suggesting a significant correlation between taste performance and market success.

Nectar’s report shows that taste parity is now achievable in some categories. What does this mean for dairy-free manufacturers trying to scale into mainstream adoption?

Cotto: Taste parity is no longer aspirational — it’s achievable. Califia Farms Oat Barista Blend achieved statistically significant taste parity with Horizon Whole Milk in blind testing, and three additional products showed no significant difference from their dairy benchmarks. That’s a meaningful signal for the industry.

Caroline Cotto: Plant-based matrices simply don’t replicate the complexity of dairy flavor — shaped by fat composition, fermentation, and emulsification — by default.What this tells manufacturers is that the formula for success exists and is replicable. Category leaders in barista milk, creamer, milk, sour cream, and cream cheese have all closed the gap to within 0.4 points of dairy benchmarks on overall liking. And our data show a statistically significant correlation between taste performance and market penetration.

Caroline Cotto: Plant-based matrices simply don’t replicate the complexity of dairy flavor — shaped by fat composition, fermentation, and emulsification — by default.What this tells manufacturers is that the formula for success exists and is replicable. Category leaders in barista milk, creamer, milk, sour cream, and cream cheese have all closed the gap to within 0.4 points of dairy benchmarks on overall liking. And our data show a statistically significant correlation between taste performance and market penetration.

Milk, the best-tasting category, has 15 times the market share of cheese, the worst-tasting. The opportunity cost of underperforming on taste is enormous. Manufacturers who invest in closing that gap aren’t just improving product quality — they’re unlocking market share.

The data highlights flavor as the biggest barrier. Why has this remained such a persistent challenge for dairy-free formulations?

Cotto: Dairy flavor is extraordinarily complex. It’s the product of fat composition, fermentation, emulsification, and more — a web of chemistry that took millennia of agricultural selection and centuries of artisanal refinement to develop. Plant-based matrices simply don’t replicate that complexity by default.

What our data show is that the most common failure modes are specific and addressable: dairy-free products consistently underperform on richness, and they carry off-flavors and off-aftertastes that participants notice and dislike. Flavor was mentioned as a dislike by 60% of participants for the average dairy-free product, compared to 51% for dairy benchmarks, which also generate flavor dislikes, just different ones.

The gap is real, but it’s not insurmountable. The persistent challenge has been that many formulations have been optimized for other attributes, such as nutrition, ingredient deck, and cost. The data suggest that doubling down on flavor, especially reducing off-flavor notes that consistently disappoint consumers, may have massive dividends.

Categories like mozzarella, yogurt, and butter are still significantly behind — what are the technical hurdles holding these back?

Cotto: Each category has its own distinct set of challenges. In mozzarella, the issues are both flavor and texture — participants flagged it for sticking to teeth, lacking stretchiness, and gumminess, in addition to off-flavor and insufficient richness. Achieving the melt, pull, and browning behavior of casein-based cheese without casein remains one of the hardest problems in dairy-free R&D. The gap between the dairy-free leader and the dairy benchmark in mozzarella was 1.4 points, the largest of any category we tested by far.

Yogurt’s challenge is more flavor-forward. Off-aftertastes and off-flavors dominate the dislike responses, and the category also struggles with appearance attributes like whiteness and brightness that consumers associate with quality.

Butter presents a different problem. It’s fundamentally a fat delivery system, and replicating the specific flavor profile of dairy fat, including its characteristic diacetyl notes, while avoiding artificial or chemical off-notes, is genuinely difficult with plant-based fats. All three categories need formulation breakthroughs, not just incremental tweaks, and there is still white space for new leader products to emerge in these categories.

Many companies focus on clean label and nutrition, but your findings suggest these have a limited impact on liking. Are brands prioritizing the wrong things?

Cotto: The data are pretty clear on this. With the exception of protein, macronutrients showed weak or no correlation with overall liking, and there were no moderate or strong correlations between major ingredients and purchase intent or liking.

Omnivore and flexitarian participants tested alt-dairy products in coffee (barista milk), pizza (mozarella), and bagels (cream cheese) at restaurants in San Francisco and New York City (Image credit: Nectar).That doesn’t mean nutrition doesn’t matter. Some 48% of consumers strongly agree that health factors into their purchasing decisions, and health-oriented consumers are significantly more likely to purchase dairy-free products. But nutrition is a purchase driver at the consideration stage, not a driver of sensory satisfaction after the first bite.

Omnivore and flexitarian participants tested alt-dairy products in coffee (barista milk), pizza (mozarella), and bagels (cream cheese) at restaurants in San Francisco and New York City (Image credit: Nectar).That doesn’t mean nutrition doesn’t matter. Some 48% of consumers strongly agree that health factors into their purchasing decisions, and health-oriented consumers are significantly more likely to purchase dairy-free products. But nutrition is a purchase driver at the consideration stage, not a driver of sensory satisfaction after the first bite.

The risk for brands is investing heavily in clean label positioning or protein fortification while underinvesting in the flavor work that actually determines repeat purchase. We did find that higher protein levels increase purchase intent, which tracks with stated consumer preferences — but also that added protein tends to reduce overall product performance, likely because high-protein plant ingredients often carry beany or chalky notes. That’s a real tension that brands need to navigate carefully.

The report points to richness and off-flavor reduction as key opportunities — what specific ingredient or technology approaches look most promising here?

Cotto: The opportunities our data point to map well onto some of the more promising directions we’re seeing in the ingredient space. On richness, the challenge is creating that full, coating mouthfeel and flavor saturation that consumers associate with dairy fat. Ingredient suppliers working on more sophisticated fat structuring, lipid blends, and emulsification systems are addressing this directly.

Off-flavor reduction, masking, and flavor modulation technology has advanced significantly, and fermentation-derived flavor compounds are increasingly being used to add authentic dairy character without the full fermentation process.

Enzymatic processing of plant proteins to reduce beany and grassy notes is another area that’s showing real promise. The brands winning on flavor right now are generally those making sophisticated ingredient and processing choices rather than defaulting to the cheapest available inputs.

How can the link between taste and market share impact where companies invest across R&D, marketing, and pricing?

Cotto: The taste-market share relationship is statistically significant, and the effect size is large enough that it should change how leaders allocate resources. Categories rated 1.3 or more points below their dairy benchmark have captured less than 2% of the market. That’s the cost of the taste gap.

The prioritization we’d suggest, based on the data: first, invest in sensory R&D with the explicit goal of closing the flavor gap, particularly richness and off-note reduction. Second, invest in a pricing strategy. A 25% premium prices out 43% of potential consumers compared to price parity. That’s a catastrophic market size reduction, and it compounds the taste disadvantage.

Third, align marketing to the emotional territory that drives purchase intent (joy, comfort, satiation, indulgence) rather than leading with sustainability or ethics messaging, which resonates strongly with only about 13% of the market. The brands that get all three of these right simultaneously are the ones positioned to break through.

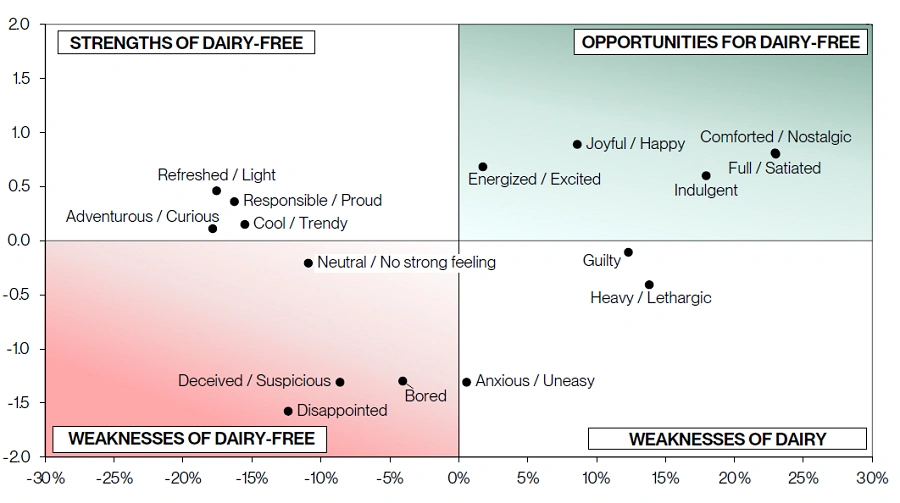

Dairy-free products perform well on health and sustainability, but sometimes lag on indulgence and comfort. How can brands bridge this emotional gap?

Cotto: This is one of the most strategically important findings in the report. Emotions like nostalgia, indulgence, satiation, and joy were significantly more associated with dairy products in our testing, and each of these was linked to a 0.6 to 0.9 point increase in purchase intent. Suspicion and disappointment, which were more commonly experienced with dairy-free products, had a very large negative impact of 1.3 to 1.6 points.

Higher prices of dairy-free products can deter consumers, with a 25% price premium excluding 43% of consumers, while an additional 25% premium reduces this by 56%, says the report.Bridging this gap requires work on two levels. The first is the product. Indulgence is primarily delivered through sensory experience, which means richer flavor, more satisfying texture, and the absence of off-notes that trigger suspicion or disappointment.

Higher prices of dairy-free products can deter consumers, with a 25% price premium excluding 43% of consumers, while an additional 25% premium reduces this by 56%, says the report.Bridging this gap requires work on two levels. The first is the product. Indulgence is primarily delivered through sensory experience, which means richer flavor, more satisfying texture, and the absence of off-notes that trigger suspicion or disappointment.

The second is brand and communication. Dairy carries enormous cultural freight: its comfort, celebration, and childhood memory. Dairy-free brands that find authentic ways to tap into those emotional registers, rather than leading with what their product isn’t, are starting to break through. It’s not about abandoning the health and sustainability story — it’s about not letting those be the only story.

What will define the next breakthrough in dairy-free, and which category is closest?

Cotto: The next breakthrough will be defined by flavor. Specifically, achieving richness and dairy-characteristic taste profiles without the off-notes that currently hold most categories back. Whoever cracks that formulation challenge at scale and at accessible price points will redefine the category.

In terms of proximity to a breakthrough, I’d point to two different types of opportunity. Cream cheese is closest to widespread competitive performance. The gap between the category leader and the dairy benchmark is relatively small, purchase intent is strong, and the application context (on a bagel, as a spread) is forgiving in ways that mozzarella on pizza is not.

The category with the most transformative upside, and the most urgent need, is mozzarella. It’s the largest cheese category globally. However, it had no Tasty Award winners in our dataset, and the leader is still 1.4 points behind the dairy benchmark. Whoever solves dairy-free mozzarella doesn’t just win a product category — they unlock the entire foodservice pizza market.

Dairy-free brands can boost consumer appeal and purchase intent by evoking emotions of joy and comfort and avoiding negative dairy-free reactions (Image credit: Nectar).

Dairy-free brands can boost consumer appeal and purchase intent by evoking emotions of joy and comfort and avoiding negative dairy-free reactions (Image credit: Nectar).